As mentioned in above, we can't explicitly attribute any of this to the EEDI requirements as they apply only to newbuilds contracted from 2013 onwards (fleet replacement running around 3% per annum), which would only have been delivered from perhaps 2014 onwards or later, while the above charts are for the whole fleet.

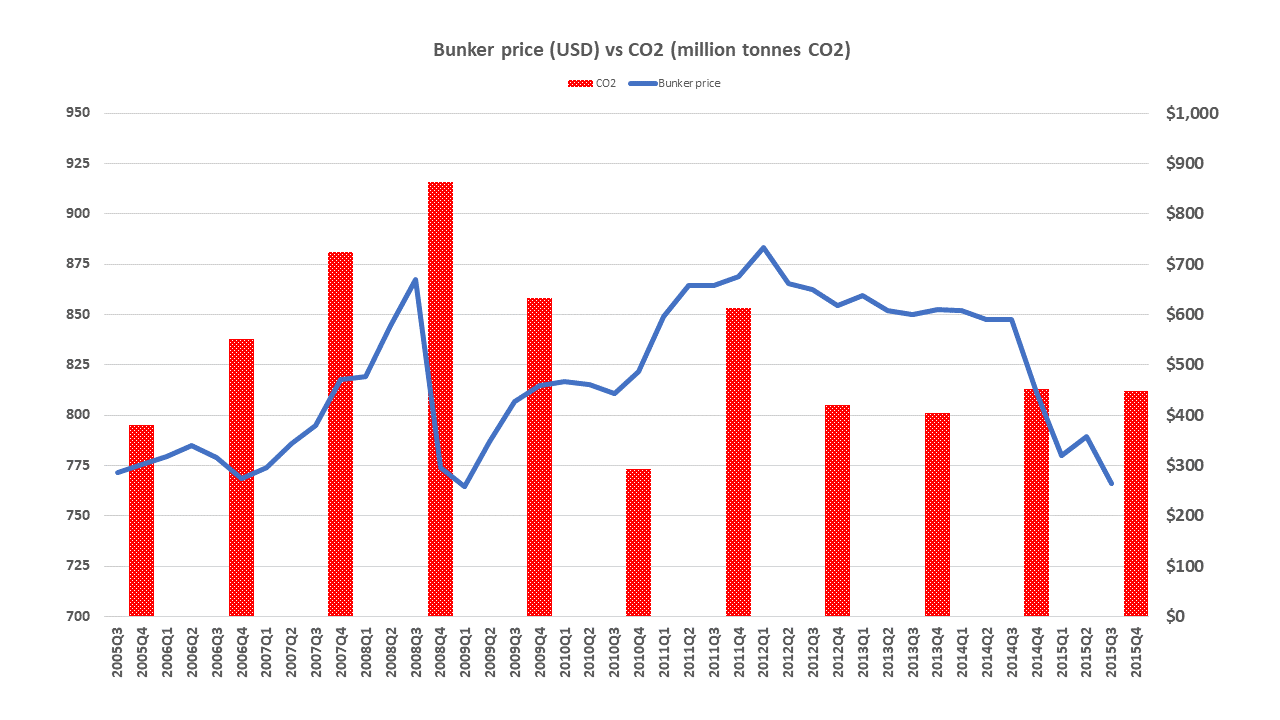

So how has shipping achieved these improvements fleet wide? The usual explanation is widespread slow steaming, and this has undoubtedly played a large part in the improvements seen to date and there are moves afoot to try to replicate this success by imposing a regulatory speed limit. However if speed were the only factor, one might expect a sharper drop in our gCO2 per tonne mile KPI followed by a plateau, unless the speed reduction was gradually applied. What other changes in the fleet would result in a gradual drop?

There have certainly been investment in energy saving measures – paint, hydrodynamic devices, hull optimisation, improved engine efficiencies, propeller optimisation, hull cleaning and so on, though it should be noted that shipping companies have found it challenging to quantify the benefits, even with big data.

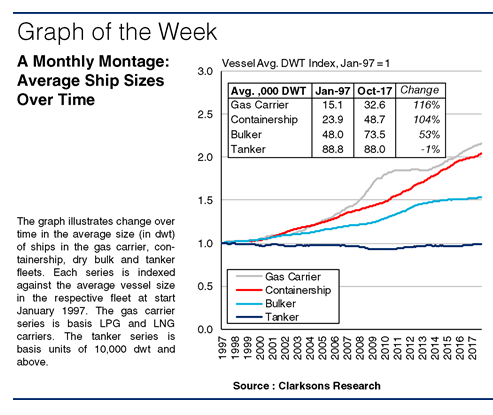

An often overlooked factor is ship size. Clarksons Research helpfully produced some analysis recently showing that average ship sizes had increased over the last 20 years; in the case of gas carriers and container ships the average size had doubled in that time and were still growing. Bulk carriers were 50% larger, and only tankers were fairly constant, as one might expect. The Panama canal widening has also opened up possibilities for larger panamax ships with increased beam and reduced ballast designs.